Cape Coral Flood Zones Explained: What Buyers Need to Know Before Making an Offer

Cape Coral Flood Zones Explained: What Buyers Need to Know Before Making an Offer

By Sheri Harris, Integrity 1st Group | eXp Realty — Cape Coral, FL

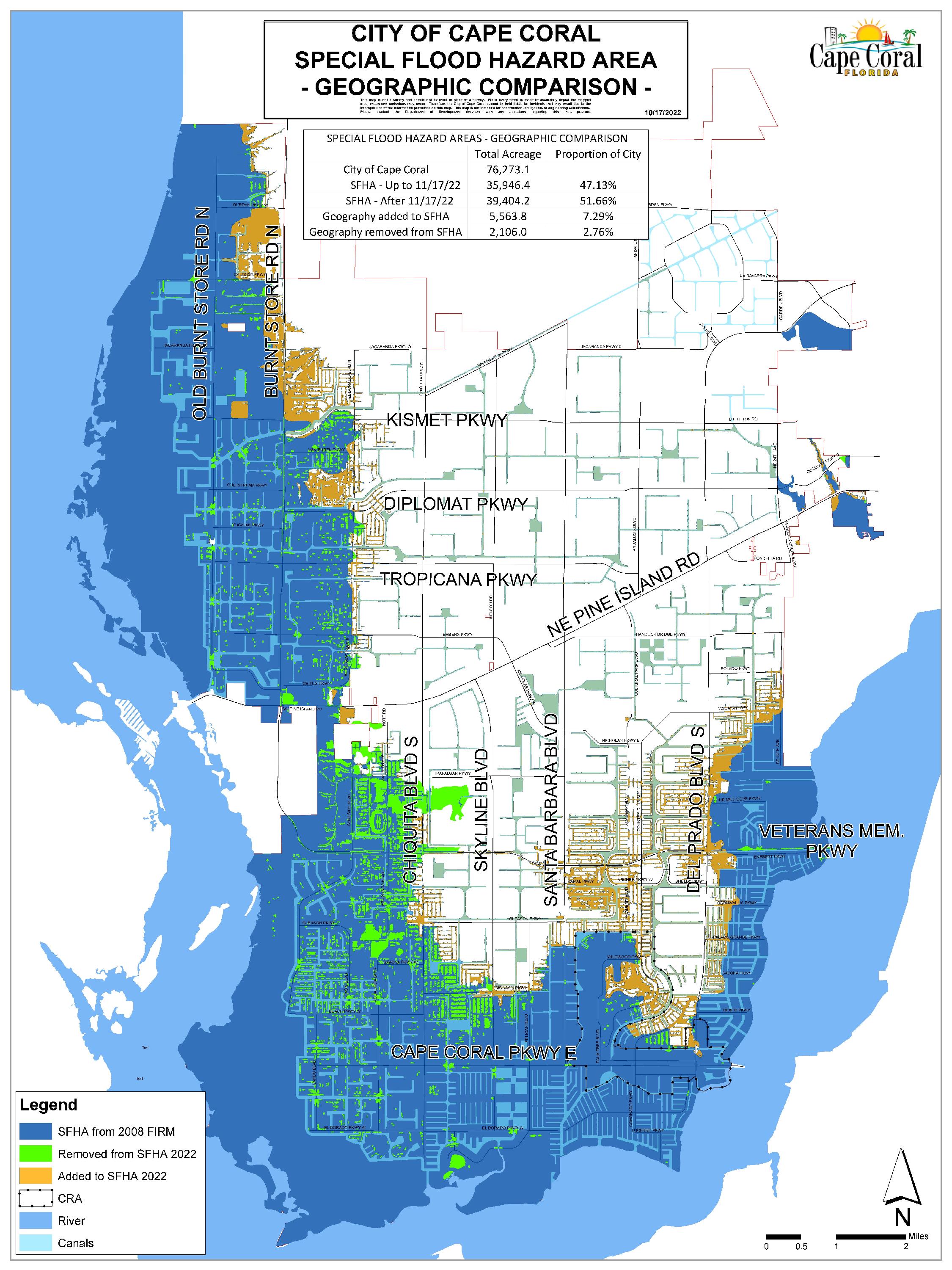

Cape Coral Special Flood Hazard Area - Geographic Comparison

Flood zones are the first thing that confuses buyers looking at Cape Coral. Understandably so. You pull up a property on Zillow, fall in love with the canal view and the pool cage, and then someone mentions that more than 85% of Cape Coral sits in some form of FEMA flood zone. That number sounds alarming until you understand what it actually means.

Not all flood zones are the same. Some carry mandatory insurance requirements and real financial weight. Others are more of a technicality. Here's what each one means in practical terms for someone buying a home here.

The zones you'll actually encounter in Cape Coral

FEMA updated Cape Coral's flood maps in November 2022 — the first major revision in 14 years. So if you're looking at flood zone information that predates late 2022, it's outdated. The current maps are what lenders and insurance companies use.

AE Zone. This is the big one. AE zones are Special Flood Hazard Areas where FEMA has calculated specific base flood elevations (BFEs). If your home is in an AE zone and you have a mortgage, your lender will require flood insurance. Period. There's no way around it. A large portion of Cape Coral's waterfront properties, especially those along gulf access canals and closer to the Caloosahatchee River, fall into AE zones.

The base flood elevation number matters a lot here. It tells you how high floodwaters are expected to rise during a 1% annual chance flood (sometimes called the "100-year flood," though that name is misleading — it doesn't mean it only happens once a century). New construction in Cape Coral must be built above the BFE, and homes that sit well above their zone's BFE typically pay lower flood insurance premiums.

VE Zone. This is the coastal high hazard area. In Cape Coral, VE zones are mostly along the southern and western edges near the river and barrier islands. These areas face both flooding and wave action during storms. Building requirements are stricter and insurance premiums are higher than AE zones.

X Zone. This is the one that makes people relax too quickly. X zones are areas of moderate to minimal flood risk. If your property is in an X zone, your lender won't require flood insurance. But "not required" and "not needed" are different things. FEMA's own data says 25% of flood insurance claims come from properties outside the Special Flood Hazard Areas. Cape Coral is flat, low-lying, and gets about 55 inches of rain per year. Heavy afternoon thunderstorms can flood streets and yards in X zones just as easily as anywhere else.

AH Zone. Less common, but it exists in parts of Cape Coral. These are areas with shallow flooding, usually one to three feet, during a base flood event. Mandatory insurance applies.

What this means for your wallet

Flood insurance costs in Cape Coral depend on your specific property's zone, elevation, age, and construction type. There's no single number that applies everywhere, but here's the general picture.

FEMA now uses Risk Rating 2.0, which prices policies based on individual property characteristics rather than just the flood zone on the map. That means two houses across the street from each other can have very different premiums if one is elevated higher or was built more recently.

Cape Coral participates in FEMA's Community Rating System (CRS) at a Class 5 level. The city has held this rating since 2010, and it nearly lost it in 2024 after some disputes with FEMA following Hurricane Ian. The city submitted a corrective action plan and retained the rating. The practical benefit: homeowners in AE and VE zones get a 25% discount on NFIP flood insurance. Properties in X zones get a 10% discount. Across the city, those CRS discounts save property owners roughly $15 million a year in aggregate.

For a typical non-beachfront home in Cape Coral, homeowners insurance runs around $3,100 to $3,600 per year. Flood insurance is separate and additional. In AE zones, NFIP policies commonly range from $1,000 to $4,000+ annually depending on elevation and structure details. In X zones, policies are cheaper since they're optional. New construction homes built to current code and above BFE tend to see the lowest premiums.

When you're running numbers on a Cape Coral purchase, always budget homeowners insurance and flood insurance as two separate line items. I've had buyers get surprised at closing because they assumed their homeowner's policy covered floods. It doesn't. In Florida, it never does.

The split-zone problem

Here's something that catches people off guard. After the 2022 map update, some properties ended up with their house in one zone and their pool, lanai, or backyard in another. A home's main structure might sit in an X zone — no mandatory flood insurance — but the pool cage extends into an AE zone. If you have a mortgage, some lenders will still require flood insurance in that situation because part of the property is in a high-risk zone.

It's fixable. If your home's finished floor is above the BFE, you can hire a surveyor to get an elevation certificate and apply to FEMA for a Letter of Map Amendment (LOMA). A LOMA officially reclassifies your structure out of the Special Flood Hazard Area. The process takes some time and a few hundred dollars for the survey, but it can eliminate a mandatory flood insurance requirement. Your realtor should flag this during the buying process, not after closing.

How to check a property's flood zone before you offer

The City of Cape Coral has a free online GIS tool where you can plug in any address and see its flood zone, base flood elevation, and elevation certificate (if one exists for buildings constructed after 1993). Go to the city's website and search under the development services section for the flood zone lookup tool.

You can also use the city's partnership with Forerunner, a third-party tool that shows flood zone, BFE, design flood elevation, and links to existing elevation certificates.

For anything built before 1993, there may not be an elevation certificate on file. In that case, you'd need to order a new one from a licensed surveyor. This typically costs $300 to $500 and is worth every dollar if you want to know exactly where you stand before making an offer.

Elevation is the variable that matters most

Two homes in the same flood zone can have wildly different insurance costs based on elevation. A home built in 2023 at 9.5 feet on fill dirt in an AE zone with a BFE of 8 feet will pay far less than a 1985 home in the same AE zone sitting at 6 feet. Under Risk Rating 2.0, FEMA weighs distance to water, property elevation relative to BFE, and the type of flood source (river, ocean, rainfall) when pricing policies.

New construction in Cape Coral is built to current Florida Building Code standards, which require the lowest floor to be above the base flood elevation plus freeboard (usually one to two additional feet). That's why new builds almost always have lower flood insurance premiums than older homes in the same neighborhood. It's one of the less obvious advantages of buying new construction here.

The bottom line for buyers

Flood zones shouldn't scare you away from Cape Coral. Most of Southwest Florida sits in some kind of flood zone, and the city's CRS participation means you're getting better insurance discounts than many neighboring communities. But you need to do your homework on a specific property before writing an offer.

Check the flood zone. Check the elevation. Get a flood insurance quote before you commit. Factor that annual cost into your budget alongside your mortgage payment, homeowners insurance, and property taxes. If you do that math upfront, there won't be any surprises.

Sheri Harris is the Team Leader of Integrity 1st Group, brokered by eXp Realty, based in Cape Coral, FL. Her team specializes in Cape Coral waterfront properties, new construction, and helping buyers relocate to Southwest Florida. Contact the team at (239) 471-2550 or visit integrity1stgroupswfl.com.

Categories

Recent Posts